OPRT (Oportun Financial)

Executive Summary

Oportun is a distressed lender that lends to underbanked borrowers through personal loans (for rental deposits and purchases) and credit cards with an average annual interest rate of around 30%. A combination of mismanagement (bloated cost structure) and bad macro (increased charge-offs) led to the stock price decreasing by 75% since the IPO in 2019. The company is currently trading at half the tangible book value, with competitors earning 6% to 30% ROE through the cycle and Oportun itself earning above 12%-20% ROE in 2016, 2018, 2019.

Under pressure from activists, the costs have significantly decreased and are expected to decrease further in 2024. The charge-offs are likely to decrease as there has been a tightening of underwriting standards, which is not in the financials yet as the majority of the book still has pre-tightening loans. A competitor with a shorter duration of the loan book has already seen its charge-offs significantly decline, and ROE return to 15%.

Management forecasts a decrease in costs of 60mln of next year by the end of next year, by decreasing corporate staff, which increased as the company was pursuing various fintech initiatives and is not necessary for the primary lending business. With no change in the charge-offs that would lead to a 2X increase in the stock price, exiting at 7p/e. If together with the cost cuts, charge-offs decrease to 2020 levels, which for all the distressed lenders were still historically very high (2008 levels), the stock should be 4X the current price. If efficiency ratios come back to 2019 levels and the charge-offs are at 2020 levels the stock would be 7X the current price. That will happen if either the activist campaign is successful (25% baseline probability) or management keeps cutting costs after 2024 on their own.

The company’s story

Oportun is a distressed lender that lends to underbanked borrowers through personal loans (for rental deposits and purchases) and credit cards with an average annual interest rate of around 30%. The average loan term of around 3 years and the average loan size of 4100usd.

Oportun was founded in 2005 and IPOd in 2019 at 16usd a share. Now the stock is worth less than 4usd with a market cap of 130mln. In 2018 the company earned 120mln of net income, in 2019 - 61mln on a 2bn loan book. Since then the results deteriorated. The company pursued a number of fintech initiatives, which led to a 100mln goodwill impairment and a significantly increased cost structure. At the beginning of 2023, Findell Capital wrote a letter to the board and brought public attention to the company. Since then the costs started decreasing and the company reported that as of Q3 2023, the OpEx to Average Managed Principle Balance is 15% relative to 20.4% in Q3 2019. Two possibly more accurate measures of efficiency, which the company didn't publish, are OpEx to Aggregate Originations which is 25% as of Q3 2023, the second-highest in the last five years and costs per loan originated, which were the highest since 2019.

Following the reductions in costs, the stock price increased over 2 fold. However, later in 2023, the company was hit hard by the charge-offs and markdowns of its loan book, which resulted in net losses of 140mln in the first 3 quarters of 2023 and a significantly missed guidance in the 3rd quarter. After that, the stock reached new lows at 2.2usd. Following the reductions in costs, the stock price increased over 2 fold. However, later in 2023, the company was hit hard by the charge-offs and markdowns of its loan book, which resulted in net losses of 140mln in the first 3 quarters of 2023 and a significantly missed guidance in the 3rd quarter. After that, the stock reached new lows at 2.2usd.

Key factors

The key factors determining the success of the investment are most likely the quality of the loan book (charge-offs), interest expense and operating efficiency.

Interest Expense

Oportun funds itself via VIEs, which hold the loans that Oportun originates and borrow amortising debt against those loans. As of Q3 2023, the implied interest rate on Oportun’s borrowings is around 7.7%. The interest rate on the last issue of asset-backed notes, that Oportun issued in 2022 is 9.05%. Secured financing with a variable interest rate was mostly done at LIBOR + 3.41%, so now it’s slightly less than 9%.

World Acceptance Corp lends to more subprime borrowers at a higher interest rate and with a higher charge-off ratio. It pays around 8.5% interest on its borrowings on average and 9.8% on the revolving credit facility.

OneMain Financial which charges a lower interest rate and has lower charge-off rates has a weighted average interest cost of 5.3%. The latest issue of senior notes was done at 7.8% in December 2023. However, the latest securitised borrowing, ODART 2023-1, was done at 5.6%. We should compare OPRT borrowings to OneMain’s securitised borrowings since all of OPRT’s borrowings are securitised.

As we can see from analysing the competitors, interest rates are tied to the quality of collateral and are correlated with the charge-off rates, so the bet on the decreasing charge-off rate becomes levered, as the interest expense will likely move in the same direction as the charge-off rate.

For my base case, I will assume a 9% weighted average rate on Oportun’s borrowings, slightly more than what Oportun pays on its floating rate debt and the same as the rate on its latest financing.

Loan book

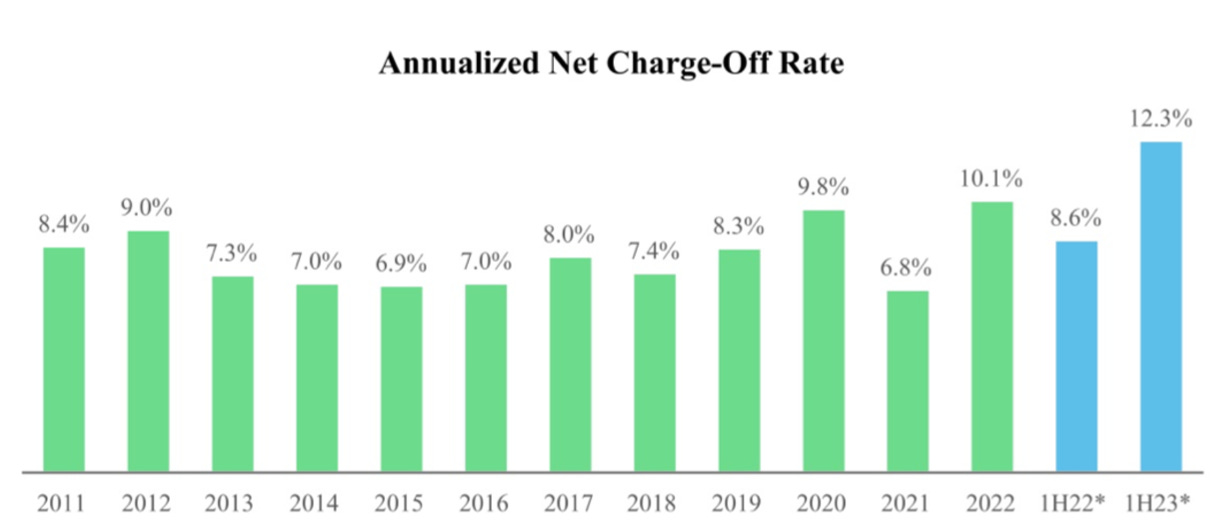

After Oportun saw a deterioration in credit quality, the company tightened the underwriting standards twice: in July and December 2022. As of Q2, the charge-offs on post-tightening Q4 2022 and Q1 2023 vintages were lower than on 2019 vintages for the respective quarters, but in Q3 2023 the net charge-offs on the Q4 2022 vintage increased to 6.1% vs 5.5% for the 2019 vintage, significantly underperforming it. As for the Q1 2023, the company changed the presentation format from net charge-offs + delinquencies to just net charge-offs, so it’s not possible to compare the dynamics of the charge-offs for the cohort that was originated after the 2 tightenings, which is probably a negative sign.

The likelihood of finding the gross yield/charge-off balance to have a satisfactory return on equity.

A long history of existence: OneMain was founded in 1912, World Acceptance in 1962, and Oportun in 2005. As mentioned earlier, each company has a slightly different niche across the credit spectrum with Oportun sitting in the middle. These companies have a very long history of existence, surviving many crises and demonstrating decent returns on capital.

Possibility for correcting mistakes: The duration of Oportun’s loan book is around 3 years, so the company doesn’t have to be stuck forever with cohorts where the yields don’t sufficiently compensate for the credit risks.

Precedents of successfully managing the charge-offs: Every lender saw their charge-off rates increase in 2022. World Acceptance which has the quickest turning portfolio (average life <1 year) has already seen the results of the tightening and saw its charge of rate drop from around 25% to around 16% and return on equity is coming back to around 15%. OneMain says that its post-tightening book has a target 6%-7% charge-off rate, however, its book is also longer than World’s so the results are not in the financials yet.

Bear Argument: OneMain and World Acceptance might be better at assessing credit worthiness of their borrowers and their long existence doesn’t necessarily imply that everyone who does the same business survives for decades. It’s possible, but Oportun has a bigger loan book than World Acceptance and has a huge amount of data on its underbanked communities, which increases the odds that it should be decent at underwriting.

Tightenings and the Loan Portfolio Size, Gross Yield.

After the July tightening, aggregate originations declined 24% Y/Y. Annualising the Q3 number for originations gives us 1.9bn originations a year. In the last five years, approximately 60% of the managed principal balance was maturing every year, which is also around 1.9bn. So at the current rate of originations, the loan book will be neither shrinking nor growing. So, as long as the average interest rate on these loans stays the same, gross interest income will be the same as this year. Historically the gross yield was roughly the same (30,5% to 32%).

Valuation Scenarios

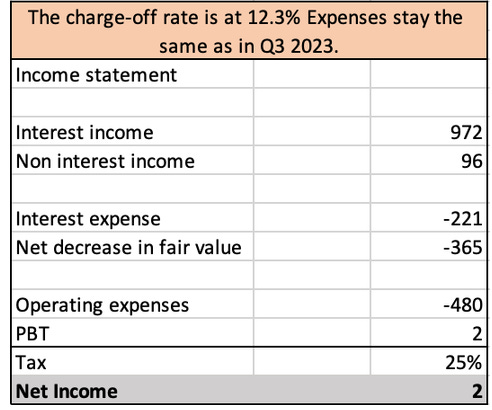

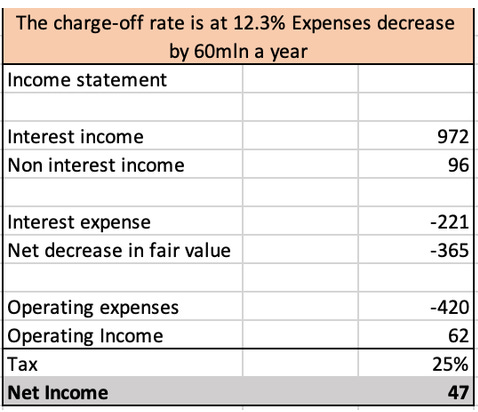

In my valuation scenarios, I will not assume any fair value marks, as they are non-cash expenses and the company doesn't have to sell loans before they mature. I will also assume that interest income stays the same, at current originations the loan book is neither shrinking nor growing and the gross yield has been roughly constant, historically.

The charge-off rate is at 12.3% as guided by management for Q4 2023 and higher than 11.8% in Q3 2023. Expenses stay the same as in Q3 2023, the interest rate on borrowings increases to 9% (slightly more than the management guides). Net income is 0 in this case.

The charge-off rate is at 12.3%. Expenses decrease by 60mln a year, due to the 18% reduction of corporate headcount. Management promised to do it until Q4 2024. Operating expenses have declined by close to 100mln since Q3 2022 already through a reduction in staff and termination of checking account and investment and retirement products. Net income is 45mln in this case. OneMain typically traded for 5-10p/e, currently trades for 9p/e and 7 forward p/e. At 7p/e Oportun would be worth 300mln (over 2x the current market cap). World Acceptance trades at 10 p/e and historically traded at much higher multiples

If the charge-off rate declines to 10.4% - 2020 rate, which was also historically elevated for all of the lenders, and expenses decrease by 60mln. Net income would be 90. At 7 p/e, that’s over 600mln mkt cap, more than 4x the current market cap

If the opex/volume of newly originated loans decreases to 2019 levels and the charge-off rate is at 2020 levels. Net income would be 140mln. At 7p/e that’s 1bn USD, or 7x current market cap

To sum up, this is a bet on expenses going down and charge-offs going down or staying the same, interest expense will be correlated to charge-offs to some extent, as the quality of collateral will change. I have given my thoughts on the charge-offs and wouldn’t bet on this driver alone, but I am leaning towards the belief that it’s a manageable situation, given that 1/3 of the book is still pre-tightening, and the competitors have a long history of existence and came out of this crisis successfully.

However, the charge-offs don’t have to decrease for the thesis to work, it’s enough for the expenses to decrease, and a path to decreasing expenses seems clear - simply decreasing the headcount, to achieve pre-corona efficiency metrics. So I believe it’s an asymmetrical investment, however, as Mr Gordon Gekko would say it’s a dog with fleas.

Risks

Management burning cash

Management can keep burning cash on fire if the company becomes profitable again. I hope that management returns to burning cash on fintech initiatives only after the profitability recovers, otherwise, the company may go bankrupt and it wouldn’t be possible for them to receive their high salaries. The CEO has a 700k base salary, a 700k possible bonus linked to adjusted net income, member growth, product growth, and digit integration (nothing about the stock price of ROIC) and 4mln USD in RSUs and options vesting over 40 years (75% - RSUs, 25% - options). Considering a low stock price relative to the earning ability of the company, the street’s expectations are low and the increase in profitability is likely to be followed by the stock price increase, and hopefully there will be time to sell the stock before management returns to burning cash. Alternatively, Findell Capital’s campaign will succeed and the management will be replaced, removing the risk. In 2023 activists had a 25% success rate at replacing officers.

Interest expense increases

Net income is very sensitive to the cost of funds. Most of Oportun’s debt consists of amortising asset-backed notes, which amortise as the consumer loans come due. So the duration of the loans is also short-term and the interest expense has already increased from 10mln in Q3 of 2021 to 25mln in Q3 of 2022 to 46mln in Q3 of 2023. However, considering the duration of the loan book is around 3 years, not all of the debt has been refinanced at higher rates and interest expense will likely increase the following quarters as more debt is refinanced. This risk is somewhat mitigated by the expected decline in interest rates in the second half of next year (the treasury yield curve is downward sloping) and tighter underwriting standards which will probably lead to lower borrowing costs since the quality of the collateral increases.

Macro

If interest rates increase, the cost of financing will increase which will significantly hit net income.

Persistently high inflation or/and higher unemployment will make it more difficult for low-income borrowers to repay loans.

Unemployment hasn’t even risen for blue-collar workers and inflation has been declining, however, all lenders have seen their charge-offs significantly increase. If unemployment rises, there is a risk to Oportun’s survival. Nonetheless, the main case scenario is that interest rates are going to decline slightly and the chances of a recession in 2024 have come down substantially. In addition, wage growth is catching up with inflation, which is now lower than the wage growth: at 4.5% wage growth and 3.4% annualised inflation in December.

Conclusion

This is not a high-quality Buffett investment. However, I think, this is an asymmetrical investment, where there is a lot of pessimism baked into the stock price, assuming that the current state of affairs will continue. Expenses are likely to be cut and it’s possible to see how the charge-offs decrease. If expenses are cut as the management said the stock should be up 2x, so for a positive expected value we only need a 50% chance of that happening, this doesn’t account for the possibility of charge-offs decreasing, which are currently the highest historically and were the highest historically for World Acceptance in 2022, even surpassing 2008.